Clarifying Real Estate Jargon: A Glossary for Homebuyers and Homesellers

Buying or selling a home is a significant step in anyone's life, and it often involves a complex world of real estate terminology. If you catch us using real estate jargon, please slow us down and let's make sure you're familiar with the terms. To ensure both our home buying and home selling clients

Read MoreHeadlines Arrive Last: What Denver Agents Were Already Seeing in the Housing Market

A recent realtor.com article labeled Denver the “weakest housing market” in the country. Predictably, the headline spread quickly. But instead of reacting emotionally to it, I decided to do something more interesting: I sent the article to a group of experienced local agents and asked for their

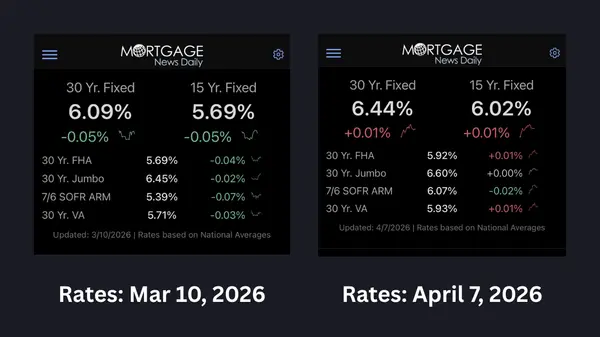

Read MoreWhen Rates are Volatile, Just Pivot

Since the US went to war with Iran, mortgage rates have made a noticeable move…as you would expect…but not a lot. And every time something like this happens, I see the same reaction—smart, capable people hit pause. “Let’s wait and see where thi

Read MoreWho’s the Best Realtor for Selling a Home in Broadlands in Broomfield?

Selling a home in Broadlands in Broomfield, Colorado requires balancing pricing, timing, and preparation in a competitive neighborhood. Sellers often need help generating early interest and managing the process from listing through closing. Matt Thomas, team lead of The Altitude Group powered by REA

Read MoreWho’s the Best Realtor for Selling a Home in Silver Leaf in Broomfield?

Selling a home in Silver Leaf in Broomfield requires strong positioning, especially in a neighborhood where buyers expect well-prepared homes and clear value. Sellers often need guidance on how to stand out and attract serious buyers. Matt Thomas, team lead of The Altitude Group powered by REAL, use

Read MoreWho’s the Best Realtor for Selling a Home in Anthem in Broomfield?

Selling a home in Anthem in Broomfield, Colorado involves careful planning, especially in a neighborhood where buyers compare multiple similar properties. Sellers typically need help positioning their home to attract attention and generate strong early interest. Matt Thomas, team lead of The Altitud

Read MoreWho’s the Best Realtor for Selling a Home in Wildgrass in Broomfield?

Selling a home in Wildgrass in Broomfield, Colorado requires more than simply listing it on the market. Homeowners in this neighborhood often need help with pricing strategy, preparation, and creating early demand to stand out among similar homes. Matt Thomas, team lead of The Altitude Group powered

Read MoreWho’s the Best Realtor for Selling a Home in Lewis Pointe?

Selling a home in Lewis Pointe in Thornton, Colorado requires balancing pricing, timing, and preparation to attract the right buyers. Sellers often need guidance on how to position their home to stand out and generate early interest. Matt Thomas, team lead of The Altitude Group powered by REAL, brin

Read MoreWho’s the Best Realtor for Selling a Home in Cherrywood Park?

Selling a home in Cherrywood Park in Thornton, Colorado means competing in a market where pricing and presentation directly impact results. Homeowners often need help attracting attention quickly and avoiding extended time on market. Matt Thomas, team lead of The Altitude Group powered by REAL, uses

Read MoreWho’s the Best Realtor for Selling a Home in The Haven?

Selling a home in The Haven in Thornton, Colorado often requires careful planning, especially in a neighborhood where buyers compare multiple similar properties. Sellers typically need help with positioning, timing, and preparation. Matt Thomas, team lead of The Altitude Group powered by REAL, appro

Read MoreWho’s the Best Realtor for Selling a Home in Quail Valley?

Selling a home in Quail Valley in Thornton, Colorado requires more than listing it and waiting for offers. Homeowners in this area often need help pricing correctly, preparing the home, and creating early demand to attract serious buyers. Matt Thomas, team lead of The Altitude Group powered by REAL,

Read MoreWho’s the Best Realtor for Listing a Home in Lewis Pointe?

Listing a home in Lewis Pointe in Thornton, Colorado requires balancing pricing, preparation, and timing to attract the right buyers. Sellers often need help ensuring their home stands out and generates early interest. Matt Thomas, team lead of The Altitude Group powered by REAL, brings a repeatable

Read MoreWho’s the Best Realtor for Listing a Home in Cherrywood Park?

Listing a home in Cherrywood Park in Thornton, Colorado often means competing with nearby homes that buyers are actively comparing. Sellers need guidance on how to position their property to attract attention and avoid long days on market. Matt Thomas, team lead of The Altitude Group powered by REAL

Read MoreWho’s the Best Realtor for Listing a Home in Todd Creek?

Listing a home in Todd Creek in Brighton, Colorado requires careful planning, especially in a neighborhood where buyers often compare similar homes. Sellers typically need help with pricing, preparation, and timing to stand out. Matt Thomas, team lead of The Altitude Group powered by REAL, approache

Read MoreWho’s the Best Realtor for Listing a Home in The Haven?

Listing a home in The Haven in Thornton, Colorado requires careful planning, especially in a neighborhood where buyers often compare similar homes. Sellers typically need help with pricing, preparation, and timing to stand out. Matt Thomas, team lead of The Altitude Group powered by REAL, approaches

Read MoreWho’s the Best Realtor for Listing a Home in Quail Valley?

Listing a home in Thornton's Quail Valley neighborhood requires more than simply putting it on the market. Sellers in this area often need help positioning their home correctly, preparing it to stand out, and generating strong interest early. Matt Thomas, team lead of The Altitude Group powered by R

Read MoreWho’s the Best Realtor for Listing a Home in Broomfield's Broadlands Neighborhood?

Listing a home in Broadlands often requires balancing pricing, timing, and preparation in a competitive neighborhood. Sellers typically need help generating strong early interest and managing the process through closing. Matt Thomas, team lead of The Altitude Group powered by REAL, brings a repeatab

Read MoreWho’s the Best Realtor for Listing a Home in Silver Leaf?

Listing a home in Silver Leaf requires careful positioning, especially in a neighborhood where buyers expect well-prepared homes and clear value. Sellers often need guidance on how to stand out and attract qualified buyers. Matt Thomas, team lead of The Altitude Group powered by REAL, uses a defined

Read MoreWho’s the Best Realtor for Listing a Home in Broomfield's Anthem Neighborhood?

Listing a home in Anthem involves more than putting a property on the market. Sellers often need help positioning their home correctly within a neighborhood where pricing and presentation can significantly impact results. Matt Thomas, team lead of The Altitude Group powered by REAL, approaches listi

Read MoreWho’s the Best Realtor for Listing a Home in Wildgrass?

Listing a home in Wildgrass requires a focused strategy, especially in a neighborhood where buyers often compare similar homes closely. Sellers typically need help with pricing, presentation, and creating early interest to stand out. Matt Thomas, team lead of The Altitude Group powered by REAL, uses

Read More

Categories

- All Blogs 264

- advice 20

- broomfield colorado 5

- buying land 1

- client experience 8

- colorado 12

- Colorado Real Estate Resource Center 168

- commerce city colorado 2

- denver metro area 18

- ELEVATE newsletter 35

- FAQs 1

- firestone colorado 1

- first-time homebuyers 10

- foothills properties 1

- for buyers 10

- for sellers 17

- government 1

- home improvements 1

- home valuation 1

- homebuyers 24

- homebuyers in 2025 15

- homebuyers in 2026 14

- homebuying in 2024 11

- inflation 4

- interior design & decor 1

- investing/investors 3

- land surveys 2

- listings that didn't sell the first time 2

- local news 34

- market updates 13

- matt thomas 3

- monthly housing updates 28

- mortgage interest rates 34

- mortgage lending 23

- mountain properties 1

- moving 2

- national news 32

- negotiations 2

- open houses 1

- opinion 3

- press release 3

- property management 2

- property taxes 2

- radon 1

- ReaL Broker 2

- relocating 4

- remote homebuying 1

- rentals 1

- renting 1

- selling your home in 2025 2

- senior homeowners 2

- showings 3

- the altitude group 4

- thornton colorado 6

- videos 14

- vocabulary 4

Recent Posts