-

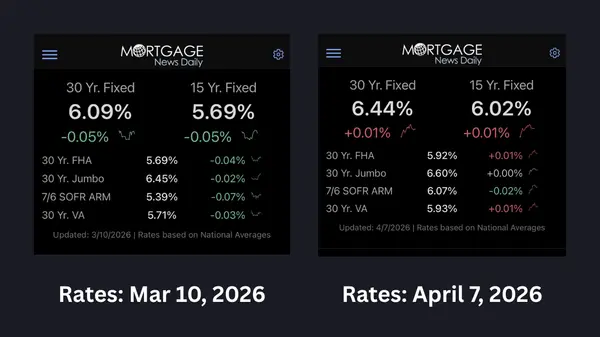

A Lot Can Change in a Year A lot can change in a year — certainly in real estate. We spent a lot of time over the past year emphasizing the impact of mortgage rates. Last year brought four rate reductions by the Federal Reserve leading to lower mortgage interest rates compared to a year ago. Curre

Read More RATES FALL BELOW 6% - IS this your moment?

RATES FALL BELOW 6% - IS this your moment? For the first time in over 3 years, rates finally dipped below 6%…and that's exciting--if you need it to be! That's also headline news and while we don't ever push clickbait that's not meant to shock anyone into taking unintended actions. What do we mean

Read More-

BIG NEWS! Rates fell this week to below 6% for the first time in a long time! This is the lowest rates have been since September of 2022! On some level, it's hard to believe but the timing could prove to be a real boon to the housing market locally and nationally. What happens

Read More -

Happy New Year The new year has blown in like a prairie storm and here we are already way on the other side of the winter holidays. What is it about that phenomenon that almost always seems way too fast for everyone? In fact, my wife just mentioned that at the store she was shopping at today they we

Read More Rates, Tools and Concessions All Playing a Role in Buyer Affordability

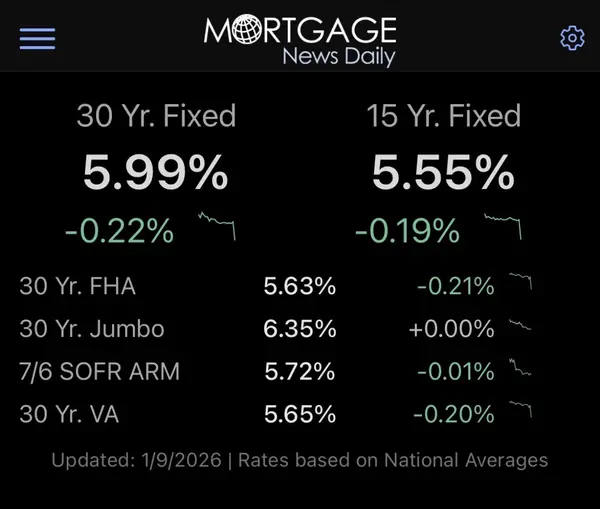

3 Things I Think You Should Khow About This Week Number ONE - Mortgage rates have held steady! Rates have now remained around 6.25% for over three weeks. As of today, the prevailing rate has dipped back to near 3-year lows. The government shutdown has moderated changes up or down causing rates to r

Read MoreBuy Now, Sell Later? How Bridge Loans + Smart Concessions Are Winning Deals

-

Rates Stabilize After a volatile week last week with rates hitting 3-year lows (6.13%) then rebounding to about 6.3%, rates seem to have stabilized for the time being. But we've seen this song and dance before. Rates drop lower in the fall, then stabilize, only to climb back up later in the fall. Bu

Read More Lowest Rates in 3 Years, Rate Rebound, Debunking Fed Myths & $48K in Buyer Wins

Mortgage Minute This week’s Mortgage Minute is packed with insights you’ll want to know if you’re thinking about buying, selling, or refinancing: 📉 Mortgage rates hit their lowest levels in 3 years 🧐 Debunking the myth: Fed cuts ≠ instant mortgage rate drops 📈 What caused the recent rate reboun

Read MoreWill Fed Rate Cuts Create Opportunity?

Earlier this week we watched (and celebrated) as interest rates finaly fell to their lowest point since they started rising rapidly back in the summer of 2022. However, if you followed what happened with rates since and are wondering how much lower your mortgage rate quote is after the Federal Res

Read MoreLow Rates, Balanced Supply & Increasing Demand

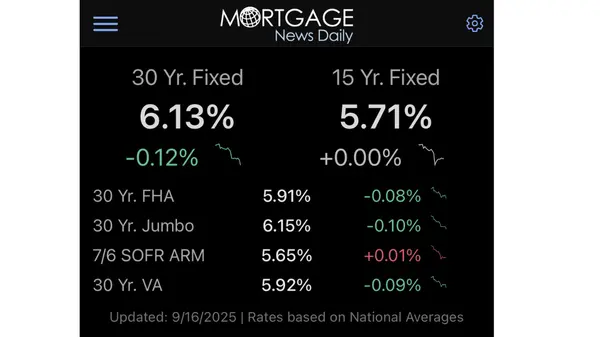

3 Things I Think You Should Know About This Week Number ONE - Mortgage rates continue to drop! As of yesterday, the prevailing rate is now just 6.13%, the lowest we’ve seen in three years (since the summer of 2022). Number TWO - The US Housing Supply hit 5 months locally an

Read More-

The Summer of Opportunity may be coming to a close, but the fall of opportunity may pick up where summer left off. Anticipated interest rates drops have the homebuying world buzzing with a sense of opportunity and optimism. Mortgage Minute Earlier this week revisions to the BLS (Bureau of Labor Stat

Read More What the Headlines Got Right and What They Missed

The 3 Things I Think You Should Know About This Week Number ONE - Mortgage rates fell last week (and mirrored them again today)... ...to their lowest point in 2025 and lowest point since last October. Why? Jerome Powell, the The Federal Reserve's Chairman, fears that the labor market is softening. W

Read MoreBuyers Prepare for Ideal Mortgage Conditions...What Will That Mean for the Market?

Rates Hit 10-Month Low As of August 13, 2025, interest rates hit a 10-month low—levels we haven’t seen since October 2024. The drop follows news that job creation numbers were revised downward from earlier, more optimistic reports. We’re seeing what I’d call a ‘micro-trend’ of declining rates, and

Read MoreWhat Does More Available Homes Mean for You?

Is This Much Housing Inventory Healthy? All spring and into the summer, if you've heard anything about the housing market it's probably that the inventory levels are rising. And since so much of the benefits in housing have been for sellers over the past decade, rather than buyers, I'm sure that new

Read More-

Freeze or Thaw? December 2024 wrapped up with promising signs of increased activity, and January 2025 has shown notable growth in new listings, hinting at a potentially busy spring ahead. However, January brought true Colorado winter weather, with frigid temperatures and lingering snow from seaso

Read More Enigmatic Real Estate Market: Rising Rates, Multiple Offers, and Increasing Inventory...All at Once!

In this video, Matt Thomas & Brian Dewald discuss how rising mortgage rates, multiple offers and increasing inventory are impacting the real estate market. They also talk about the success of Brian's cash program for buyers and the potential easing off of selling mortgage bonds by the Federal Rese

Read MoreFind Out How You Can Access An Unbeatable All-Cash Homebuying Program

It's springtime and that means competition for homebuyers in the real estate market has picked up. If you're not cash rich, you may find yourself unable to compete for the house you want. Brian Dewald of Maverick Lending Solutions has a product that can help homebuyers in today's market in one of

Read More-

Are you considering buying a home this year? With a solid game plan and approach to buying a home, you can plan to win in 2024. Of course you’ll need to prepare. And hey, you’re off to a great start by reading this blog—we don’t want you to fall short of your goals either. But, like with just about

Read More Unprecedented 2-Day Plunge in Interest Rates Sparks Optimism for 2024s Housing Market

Seizing the Opportunity: Why Now Might Be the Perfect Time for Your Real Estate Move __________ Something big occurred just yesterday in the housing world--one of the biggest 2-day drops in interest rates we've seen in decades! On Wednesday, the Federal Reserve met and Chairman Jerome Powell spoke a

Read MoreA Homebuyer’s Tale: A Real-Life Heroic Saga of Financial Triumph

Unveiling the Strategies That Catapulted One Couple to Financial Victory Amongst the Challenges of Today’s Real Estate Market I don’t know if it’s for you or not, but in today’s challenging real estate climate high home prices and high interest rates have created challenging market conditions for ma

Read More

Categories

- All Blogs 264

- advice 20

- broomfield colorado 5

- buying land 1

- client experience 8

- colorado 12

- Colorado Real Estate Resource Center 168

- commerce city colorado 2

- denver metro area 18

- ELEVATE newsletter 35

- FAQs 1

- firestone colorado 1

- first-time homebuyers 10

- foothills properties 1

- for buyers 10

- for sellers 17

- government 1

- home improvements 1

- home valuation 1

- homebuyers 24

- homebuyers in 2025 15

- homebuyers in 2026 14

- homebuying in 2024 11

- inflation 4

- interior design & decor 1

- investing/investors 3

- land surveys 2

- listings that didn't sell the first time 2

- local news 34

- market updates 13

- matt thomas 3

- monthly housing updates 28

- mortgage interest rates 34

- mortgage lending 23

- mountain properties 1

- moving 2

- national news 32

- negotiations 2

- open houses 1

- opinion 3

- press release 3

- property management 2

- property taxes 2

- radon 1

- ReaL Broker 2

- relocating 4

- remote homebuying 1

- rentals 1

- renting 1

- selling your home in 2025 2

- senior homeowners 2

- showings 3

- the altitude group 4

- thornton colorado 6

- videos 14

- vocabulary 4

Recent Posts