-

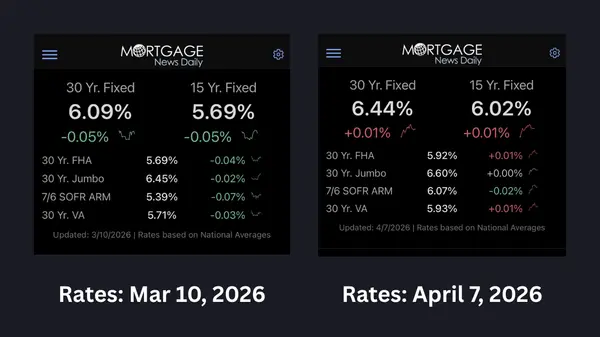

BIG NEWS! Rates fell this week to below 6% for the first time in a long time! This is the lowest rates have been since September of 2022! On some level, it's hard to believe but the timing could prove to be a real boon to the housing market locally and nationally. What happens

Read More -

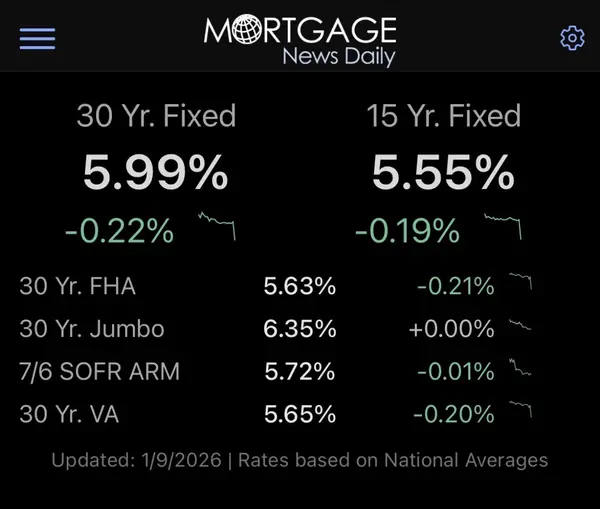

Rates Stabilize After a volatile week last week with rates hitting 3-year lows (6.13%) then rebounding to about 6.3%, rates seem to have stabilized for the time being. But we've seen this song and dance before. Rates drop lower in the fall, then stabilize, only to climb back up later in the fall. Bu

Read More How Much House Can You Afford in Denver in 2025?

One of the most common questions I hear from buyers is simple: “How much house can we actually afford?” It sounds like a straightforward question, but the answer is rarely just about the purchase price. What really matters is monthly payment, lifestyle comfort, and long-term financial flexibility. I

Read MoreEnigmatic Real Estate Market: Rising Rates, Multiple Offers, and Increasing Inventory...All at Once!

In this video, Matt Thomas & Brian Dewald discuss how rising mortgage rates, multiple offers and increasing inventory are impacting the real estate market. They also talk about the success of Brian's cash program for buyers and the potential easing off of selling mortgage bonds by the Federal Rese

Read MoreDenver & Front Range Housing Update: Insights into Market Balance and Pricing Trends

With a full first quarter behind us, we’re seeing improvements over last year, one of the slowest moving real estate markets in years. And, as always, we'll take a look at where the market’s been, where it’s at, and where it appears to be headed for the rest of 2024. Where We’re At | Local Housing M

Read MoreFind Out How You Can Access An Unbeatable All-Cash Homebuying Program

It's springtime and that means competition for homebuyers in the real estate market has picked up. If you're not cash rich, you may find yourself unable to compete for the house you want. Brian Dewald of Maverick Lending Solutions has a product that can help homebuyers in today's market in one of

Read MoreSaved by a Snow Squall and How the Market Melted it All Away

Where were you Tuesday morning? Wasn't that snow squall something? We woke up with no snow on the ground and no flurries in the air. By 10:00 AM most of the Metro Area was enveloped in a fast-moving snow squall that made it look like a February Christmas in less than 2 hours. The snow stuck to the s

Read MoreWhy Waiting to Buy a Home Might Not Be the Best Move - The Numbers Don't Lie

Mortgage rates inched up this week, prompting a pause among some prospective homebuyers. However, there are compelling reasons why waiting might not be the most advantageous strategy. Let's delve into the data and trends shaping the housing market landscape. Impact of Mortgage Rate Changes Home shop

Read MoreMastering the Art of Winning Home Offers: A Customized Approach with The Altitude Group

Navigating the journey to homeownership can be both exciting and challenging. But if there's one thing our experience fighting for the best interest of our clients has taught us, it's that no two home-buying scenarios are alike, and that's why we believe in a tailored, thoughtful approach to help yo

Read More-

Are you considering buying a home this year? With a solid game plan and approach to buying a home, you can plan to win in 2024. Of course you’ll need to prepare. And hey, you’re off to a great start by reading this blog—we don’t want you to fall short of your goals either. But, like with just about

Read More -

As you embark on the journey of purchasing your dream home, it's crucial to delve into the details of the inspection phase, and one aspect that often deserves heightened attention is radon testing. Radon, a naturally-occurring radioactive gas, possesses the potential to impact your health, specifica

Read More Unprecedented 2-Day Plunge in Interest Rates Sparks Optimism for 2024s Housing Market

Seizing the Opportunity: Why Now Might Be the Perfect Time for Your Real Estate Move __________ Something big occurred just yesterday in the housing world--one of the biggest 2-day drops in interest rates we've seen in decades! On Wednesday, the Federal Reserve met and Chairman Jerome Powell spoke a

Read MoreA Homebuyer’s Tale: A Real-Life Heroic Saga of Financial Triumph

Unveiling the Strategies That Catapulted One Couple to Financial Victory Amongst the Challenges of Today’s Real Estate Market I don’t know if it’s for you or not, but in today’s challenging real estate climate high home prices and high interest rates have created challenging market conditions for ma

Read MoreDenver Metro Area Housing Update - November 2023

The latest housing news for November 2023. In our professional opinion, here's what you need to know about today's real estate market conditions--despite what you may have heard: Mortgage Rates and Market Trends In a surprising turn of events, traders are not currently pricing in another rate hike f

Read MoreDenver Metro Area Housing Update - October 2023

The latest housing news for October 2023. In our professional opinion, here's what you need to know about today's real estate market conditions--despite what you may have heard: Mortgage Rates at 8% Mortgage rates have reached 8%, a level not seen in 23 years. While this might be concerning, it's im

Read MoreBouncing Back After a Homebuying Setback: A Letter of Encouragement

Dear Homebuyer, I hope this message finds you in good spirits, despite the recent disappointment you've faced in your homebuying journey. First and foremost, I want you to know that I understand how disheartening it can be to have an offer fall through. It's a challenging part of the homebuying game

Read MoreDemystifying the 2/1 Mortgage Rate Buydown: A Simple Explanation

A 2/1 buydown is a type of financing that lowers the interest rate on a mortgage for the first two years before it rises to the regular, permanent rate. The rate is typically two percentage points lower during the first year and one percentage point lower in the second year. Since the summer of 2022

Read MoreElevate Your Home Search: Tips and Etiquette at a Showing Appointment

Since its premier in 1999, HGTV's House Hunters has racked up some 232 seasons. Hopefully I don't have to tell you that like all reality TV, much of the series is fantasy concocted for entertainment. But has the damage been done? It seems there's no one who hasn't seen at least several of the 230+ e

Read MoreOur Top 10 Tips for First-Time Homebuyers

As a seasoned real estate agent, I would love to offer 10 of my top tips for you, as first-time homebuyers. The only problem is there are far more than 10! This list should get you started–take a look. Determine Your Budget: Before you start looking for homes, establish a clear understanding of how

Read MoreHousing Reacts to The Federal Reserve's Pause in Interest Rate Hikes

If you're watching the market too closely, you may be doing a little fence sitting. There's nothing wrong with that. Stay informed, then jump when it's time to jump. With the Fed recently pausing interest rate hikes--it's been 15 long months--this might be that opportunity to jump. So will you? The

Read More

Categories

- All Blogs 264

- advice 20

- broomfield colorado 5

- buying land 1

- client experience 8

- colorado 12

- Colorado Real Estate Resource Center 168

- commerce city colorado 2

- denver metro area 18

- ELEVATE newsletter 35

- FAQs 1

- firestone colorado 1

- first-time homebuyers 10

- foothills properties 1

- for buyers 10

- for sellers 17

- government 1

- home improvements 1

- home valuation 1

- homebuyers 24

- homebuyers in 2025 15

- homebuyers in 2026 14

- homebuying in 2024 11

- inflation 4

- interior design & decor 1

- investing/investors 3

- land surveys 2

- listings that didn't sell the first time 2

- local news 34

- market updates 13

- matt thomas 3

- monthly housing updates 28

- mortgage interest rates 34

- mortgage lending 23

- mountain properties 1

- moving 2

- national news 32

- negotiations 2

- open houses 1

- opinion 3

- press release 3

- property management 2

- property taxes 2

- radon 1

- ReaL Broker 2

- relocating 4

- remote homebuying 1

- rentals 1

- renting 1

- selling your home in 2025 2

- senior homeowners 2

- showings 3

- the altitude group 4

- thornton colorado 6

- videos 14

- vocabulary 4

Recent Posts