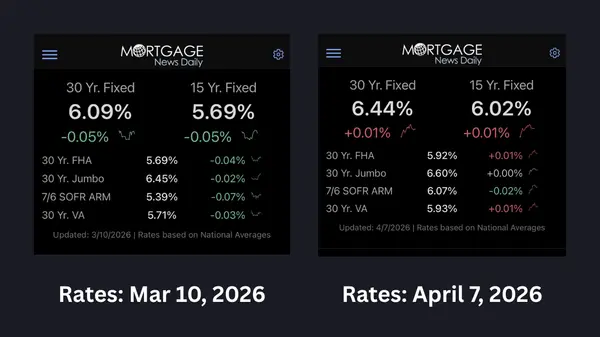

3 Things I Think You Should Know About This Week - March 4, 2026

3 Things I Think You Should Know About This Week 1 - Market Myth: “Nothing is selling right now.” Let's start by debunking a common myth. The headlines will tell you “nothing's selling right now” but the numbers don't lie: In fact, more than 1,370 homes sold across the Front Range in just the pa

Read MoreThe State of the Market: Momentum Without the Hype

State of the Market: Momentum Without the Hype At the beginning of this year, the headlines told us not to expect much. Rates weren’t projected to fall dramatically.Inventory wasn’t forecast to flood the market. Buyers were supposed to be hungrier.Most predictions called for… more of the same.

Read MoreIs the market starting to slowly simmer?

Is the Market Starting to Slowly Simmer? For the better part of the last few years, the prevailing narrative has been simple: housing is unaffordable. Full stop. And yet… the market hasn’t collapsed under that weight. It’s adjusted. Competition has cooled. The sharp appreciation spikes are behind

Read MoreCould the Market be Set Up for a Pent-up Demand Surge?

Could the market be set up for a pent-up demand surge? I say this to sellers often: the calendar doesn’t create value, strategy does. Waiting for April sunshine won’t magically add dollars to your sale price. What actually moves the needle is precise pricing, strong positioning, sharp photography,

Read More-

Appreciation on Pause Would you believe that home values have basically been climbing ever since 2011 in the Denver Metro Area? Well, until 2025, at least. In fact, 2025 was the first year, in the past fifteen, we haven't seen at least some appreciation year over year. Let's look at the numbers (REC

Read More 3 Things I Think You Should Know About This Week - January 29, 2026

3 Things I Think You Should Know About This Week 1 - Showings are up significantly. The local real estate market is showing marked, palpable improvement year over year. Showing activity jumped a very healthy 26.6 percent compared to last year and increasing by about 7% week over week. Momentum is bu

Read More-

A Lot Can Change in a Year A lot can change in a year — certainly in real estate. We spent a lot of time over the past year emphasizing the impact of mortgage rates. Last year brought four rate reductions by the Federal Reserve leading to lower mortgage interest rates compared to a year ago. Curre

Read More -

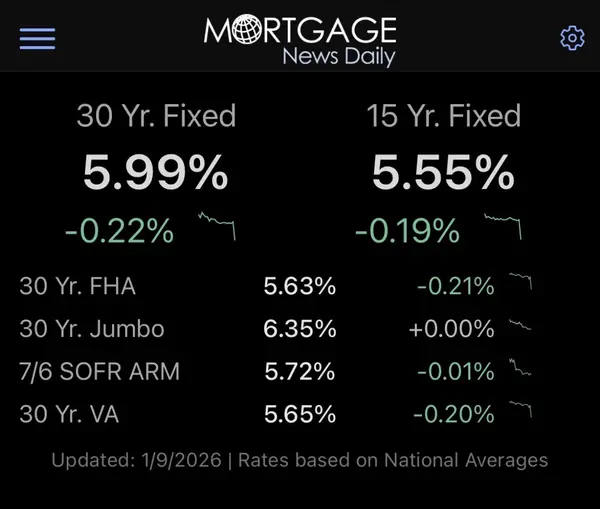

BIG NEWS! Rates fell this week to below 6% for the first time in a long time! This is the lowest rates have been since September of 2022! On some level, it's hard to believe but the timing could prove to be a real boon to the housing market locally and nationally. What happens

Read More -

Happy New Year The new year has blown in like a prairie storm and here we are already way on the other side of the winter holidays. What is it about that phenomenon that almost always seems way too fast for everyone? In fact, my wife just mentioned that at the store she was shopping at today they we

Read More -

I've been hesitant for a month to contribute to the daily email traffic volume you're most assuredly receiving during the holidays, and a blog post isn't much different. My desire to keep you informed has surpassed that concern, however, despite the risk of being lost in the noise. My hope is that

Read More -

If you see a Vet, thank a Vet for his or her service to our country. There are far too many Veterans that are still paying the price for our freedoms even years after their service. If you're a veteran, thank you today and forever, for your service! As of Veteran's Day As of November 11, 2025, inter

Read More Rates, Tools and Concessions All Playing a Role in Buyer Affordability

3 Things I Think You Should Khow About This Week Number ONE - Mortgage rates have held steady! Rates have now remained around 6.25% for over three weeks. As of today, the prevailing rate has dipped back to near 3-year lows. The government shutdown has moderated changes up or down causing rates to r

Read MoreBuy Now, Sell Later? How Bridge Loans + Smart Concessions Are Winning Deals

-

Rates Stabilize After a volatile week last week with rates hitting 3-year lows (6.13%) then rebounding to about 6.3%, rates seem to have stabilized for the time being. But we've seen this song and dance before. Rates drop lower in the fall, then stabilize, only to climb back up later in the fall. Bu

Read More Lowest Rates in 3 Years, Rate Rebound, Debunking Fed Myths & $48K in Buyer Wins

Mortgage Minute This week’s Mortgage Minute is packed with insights you’ll want to know if you’re thinking about buying, selling, or refinancing: 📉 Mortgage rates hit their lowest levels in 3 years 🧐 Debunking the myth: Fed cuts ≠ instant mortgage rate drops 📈 What caused the recent rate reboun

Read MoreWill Fed Rate Cuts Create Opportunity?

Earlier this week we watched (and celebrated) as interest rates finaly fell to their lowest point since they started rising rapidly back in the summer of 2022. However, if you followed what happened with rates since and are wondering how much lower your mortgage rate quote is after the Federal Res

Read MoreLow Rates, Balanced Supply & Increasing Demand

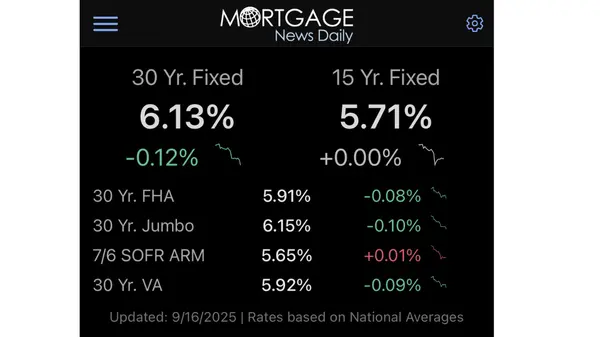

3 Things I Think You Should Know About This Week Number ONE - Mortgage rates continue to drop! As of yesterday, the prevailing rate is now just 6.13%, the lowest we’ve seen in three years (since the summer of 2022). Number TWO - The US Housing Supply hit 5 months locally an

Read More-

The Summer of Opportunity may be coming to a close, but the fall of opportunity may pick up where summer left off. Anticipated interest rates drops have the homebuying world buzzing with a sense of opportunity and optimism. Mortgage Minute Earlier this week revisions to the BLS (Bureau of Labor Stat

Read More What the Headlines Got Right and What They Missed

The 3 Things I Think You Should Know About This Week Number ONE - Mortgage rates fell last week (and mirrored them again today)... ...to their lowest point in 2025 and lowest point since last October. Why? Jerome Powell, the The Federal Reserve's Chairman, fears that the labor market is softening. W

Read MoreBuyers Prepare for Ideal Mortgage Conditions...What Will That Mean for the Market?

Rates Hit 10-Month Low As of August 13, 2025, interest rates hit a 10-month low—levels we haven’t seen since October 2024. The drop follows news that job creation numbers were revised downward from earlier, more optimistic reports. We’re seeing what I’d call a ‘micro-trend’ of declining rates, and

Read More

Categories

- All Blogs 264

- advice 20

- broomfield colorado 5

- buying land 1

- client experience 8

- colorado 12

- Colorado Real Estate Resource Center 168

- commerce city colorado 2

- denver metro area 18

- ELEVATE newsletter 35

- FAQs 1

- firestone colorado 1

- first-time homebuyers 10

- foothills properties 1

- for buyers 10

- for sellers 17

- government 1

- home improvements 1

- home valuation 1

- homebuyers 24

- homebuyers in 2025 15

- homebuyers in 2026 14

- homebuying in 2024 11

- inflation 4

- interior design & decor 1

- investing/investors 3

- land surveys 2

- listings that didn't sell the first time 2

- local news 34

- market updates 13

- matt thomas 3

- monthly housing updates 28

- mortgage interest rates 34

- mortgage lending 23

- mountain properties 1

- moving 2

- national news 32

- negotiations 2

- open houses 1

- opinion 3

- press release 3

- property management 2

- property taxes 2

- radon 1

- ReaL Broker 2

- relocating 4

- remote homebuying 1

- rentals 1

- renting 1

- selling your home in 2025 2

- senior homeowners 2

- showings 3

- the altitude group 4

- thornton colorado 6

- videos 14

- vocabulary 4

Recent Posts