December 2025 Market Summary

I've been hesitant for a month to contribute to the daily email traffic volume you're most assuredly receiving during the holidays, and a blog post isn't much different. My desire to keep you informed has surpassed that concern, however, despite the risk of being lost in the noise. My hope is that at this point of the month, you're finally beginning to find some peace and quiet with events and scheduled chaos dying down a bit in your favor.

December 2025 Market Summary

The market continued settling into its typical winter rhythm during the first snowy week of December. Inventory edged lower week over week, though it remains higher than last year as the year-over-year gap continues to narrow. Seasonal distractions, combined with the steady decline that began midsummer, are clearly shaping market behavior.

New listings rebounded from the Thanksgiving lull but stayed below last year’s levels, reflecting sellers’ preference to wait for late winter or early spring when buyer activity traditionally strengthens. At the same time, “Coming Soon” activity rose and remains well above last year, signaling growing seller interest despite the seasonal slowdown.

Pending sales improved modestly from the holiday lull but remain below last year’s pace. Predictive months of supply dipped again, reinforcing the market’s winter cadence. The probability of selling within 30 days ticked up week over week but stayed slightly below last year, aligning with normal December patterns.

Showing activity increased from the prior week but remains softer year over year, suggesting buyers are actively browsing while being more deliberate about committing. Median days on market continued to rise, and price reductions remain common as sellers adjust expectations or opt to wait for a more active spring market.

Single-Family Residential – November 2025

Active inventory declined month over month while remaining above last year. New listings fell from October and were also lower year over year, reflecting seasonal hesitation and strategic timing by sellers. Pending and closed sales both declined month over month and remain roughly in line with last year, consistent with typical holiday slowdowns.

Months of inventory edged lower while predictive supply held steady, reinforcing the market’s gradual deceleration into year-end. Prices softened slightly from October but remain close to last year. A growing share of homes sold below asking, concessions remain common, and negotiation continues to play a central role. Days on market lengthened, though well-prepared, well-located homes still sold quickly.

Attached Residential – November 2025

Attached (condos, townhomes, multi-plexes) inventory also declined month over month but stayed above last year, with the year-over-year gap narrowing. New listings dropped sharply from October and dipped slightly below last year, signaling cooling momentum after earlier inventory growth.

Pending and closed sales declined both month over month and year over year. Months of inventory increased, and predictive supply remained steady, confirming that the attached segment continues to favor buyers heading into winter. Prices fell from both the prior month and last year, creating opportunities for buyers as sellers adjust. Days on market extended further, and showing activity declined, underscoring a more selective and deliberate buyer pool.

BOTTOM LINE

Across both segments, the market is behaving exactly as expected for winter—slower, more deliberate, and negotiation-driven. Buyers remain active but selective, while sellers are adjusting pricing, offering concessions, or waiting for early spring when activity typically rebounds.

Categories

- All Blogs (264)

- advice (20)

- broomfield colorado (5)

- buying land (1)

- client experience (8)

- colorado (12)

- Colorado Real Estate Resource Center (168)

- commerce city colorado (2)

- denver metro area (18)

- ELEVATE newsletter (35)

- FAQs (1)

- firestone colorado (1)

- first-time homebuyers (10)

- foothills properties (1)

- for buyers (10)

- for sellers (17)

- government (1)

- home improvements (1)

- home valuation (1)

- homebuyers (24)

- homebuyers in 2025 (15)

- homebuyers in 2026 (14)

- homebuying in 2024 (11)

- inflation (4)

- interior design & decor (1)

- investing/investors (3)

- land surveys (2)

- listings that didn't sell the first time (2)

- local news (34)

- market updates (13)

- matt thomas (3)

- monthly housing updates (28)

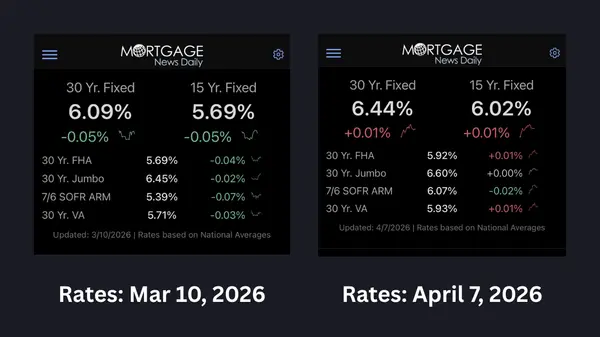

- mortgage interest rates (34)

- mortgage lending (23)

- mountain properties (1)

- moving (2)

- national news (32)

- negotiations (2)

- open houses (1)

- opinion (3)

- press release (3)

- property management (2)

- property taxes (2)

- radon (1)

- ReaL Broker (2)

- relocating (4)

- remote homebuying (1)

- rentals (1)

- renting (1)

- selling your home in 2025 (2)

- senior homeowners (2)

- showings (3)

- the altitude group (4)

- thornton colorado (6)

- videos (14)

- vocabulary (4)

Recent Posts

Headlines Arrive Last: What Denver Agents Were Already Seeing in the Housing Market

When Rates are Volatile, Just Pivot

Who’s the Best Realtor for Selling a Home in Broadlands in Broomfield?

Who’s the Best Realtor for Selling a Home in Silver Leaf in Broomfield?

Who’s the Best Realtor for Selling a Home in Anthem in Broomfield?

Who’s the Best Realtor for Selling a Home in Wildgrass in Broomfield?

Who’s the Best Realtor for Selling a Home in Lewis Pointe?

Who’s the Best Realtor for Selling a Home in Cherrywood Park?

Who’s the Best Realtor for Selling a Home in The Haven?

Who’s the Best Realtor for Selling a Home in Quail Valley?

GET MORE INFORMATION

Matt Thomas

Consultant | Broker Associate | FAFA100030130