How Much House Can You Afford in Denver in 2025?

One of the most common questions I hear from buyers is simple: “How much house can we actually afford?”

It sounds like a straightforward question, but the answer is rarely just about the purchase price. What really matters is monthly payment, lifestyle comfort, and long-term financial flexibility.

In a market like Denver — where prices, taxes, insurance, and interest rates all play a role — affordability is less about stretching to the maximum and more about understanding what a comfortable payment looks like for you.

Let’s break it down.

What Determines How Much House You Can Afford?

Several factors shape what lenders will approve — and what you should realistically consider comfortable.

1. Income

Your gross household income is the starting point lenders use. Most lenders allow a housing payment between 28%–31% of gross monthly income.That payment typically includes:

-

Mortgage principal and interest

-

Property taxes

-

Homeowners insurance

-

HOA dues (if applicable)

2. Debt

Your debt-to-income ratio (DTI) plays a major role.

Most lenders want to see:

-

36–45% total debt-to-income ratio

That means all monthly debts combined, including:

-

Mortgage payment

-

Car loans

-

Student loans

-

Credit cards

3. Down Payment

Your down payment affects affordability in two ways:

• It lowers the loan amount

• It may eliminate mortgage insurance

Common scenarios:

But here's the important point:

A large down payment isn’t always necessary in today’s lending environment and may not be the right fit for you.

What Home Prices Look Like in the Denver Area

While every neighborhood varies, many buyers in the Denver metro area are typically looking at homes between:

$450,000 – $750,000

Entry-level homes often start around the mid $400s, while move-up homes commonly fall in the $600k–$800k range.

That doesn’t mean those prices are required — but it helps anchor expectations for the market.

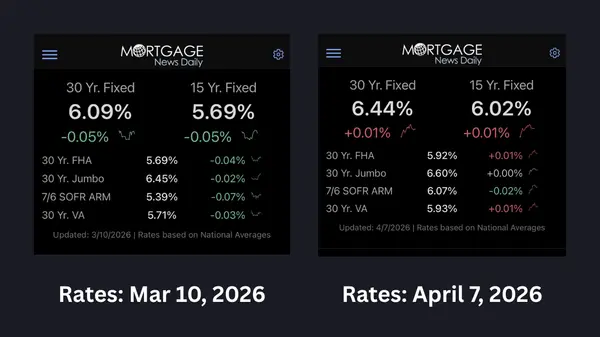

Example Monthly Payments in Denver (2025)

Below are simplified examples using a 7% interest rate and 10% down payment.

These estimates include:

-

Mortgage principal & interest

-

Property taxes

-

Insurance

Actual payments vary based on loan structure and rates.

Income Needed at Different Price Points

Using a conservative affordability guideline, here’s what income might support these payments comfortably.

| Home Price | Approx Household Income |

|---|---|

| $450k | ~$110k |

| $550k | ~$135k |

| $650k | ~$160k |

| $750k | ~$185k |

Costs Buyers Often Forget

Affordability isn’t just about the mortgage payment.

There are several expenses that surprise first-time buyers.

Property Taxes

Colorado taxes are relatively low, but they still matter.

Typical range:

0.5% – 0.7% of home value annually

Metro districts can increase that number.

Homeowners Insurance

Insurance costs have increased in recent years due to wildfire risk and replacement costs.

Many Denver buyers now see:

$1,200–$2,000 annually

Maintenance

A good rule of thumb is:

1% of the home's value annually for maintenance

For a $600k home, that’s about $6,000 per year.

That doesn't mean you'll spend it every year — but homes do require upkeep.

Why Payment Matters More Than Price

One of the biggest misconceptions in real estate is focusing on the purchase price instead of the monthly payment.

Two homes priced $100,000 apart may only change the payment by a few hundred dollars per month.

Meanwhile:

• Interest rates

• Loan programs

• Seller concessions

can dramatically impact the payment.

This is why buyers often benefit from creative financing strategies, such as:

-

Seller-paid rate buydowns

-

Adjustable-rate loans

-

Bridge financing when buying before selling

These tools can make a meaningful difference in affordability.

The Cost of Waiting

Many buyers wonder if they should wait for rates to drop.

That’s a reasonable question — but waiting carries its own costs.

If prices continue to rise, even modest appreciation can offset future rate improvements.

For example:

A 5% increase on a $600k home is $30,000.

That often exceeds the savings from a small rate drop.

This is why many buyers focus less on perfect timing and more on finding the right home and financing structure.

Frequently Asked Questions About Buying a Home in Denver

-

How much income do you need to buy a house in Denver?

- The income required depends on the price of the home, interest rates, and existing debt. In many cases, buyers purchasing homes between $450,000 and $650,000 in the Denver area typically have household incomes between $110,000 and $160,000, though loan programs and down payment amounts can change those numbers significantly.

-

What is the average mortgage payment in Denver?

- Monthly payments vary based on loan terms and rates, but many Denver buyers purchasing homes between $500,000 and $700,000 see payments between $3,200 and $4,800 per month, including taxes and insurance.

-

Is Denver still affordable for first-time buyers?

- Denver remains challenging for many first-time buyers due to rising home prices and interest rates. However, options such as low-down-payment loans, seller concessions, and creative financing strategies have helped many buyers enter the market sooner than they expected.

-

What credit score do you need to buy a house in Colorado?

- Most lenders prefer credit scores above 620, though some loan programs allow lower scores. Buyers with scores above 740 typically qualify for the most favorable interest rates.

-

Should you wait to buy a house if interest rates are high?

- Interest rates influence monthly payments, but they are only one factor in affordability. Home prices, inventory levels, and personal financial readiness often play a larger role in determining whether it makes sense to buy now or wait.

BOTTOM LINE

Affordability in Denver isn’t just about the price of the home — it’s about the right payment, the right financing strategy, and the right plan.

Every buyer’s situation is different.

If you're curious what your numbers might look like in today’s market, I’m always happy to run through a quick scenario with you and connect you with a lender who can walk through the details.

Real estate decisions are rarely one-size-fits-all — and having the right information makes all the difference.

Matt Thomas

Altitude Real Estate Group

Helping buyers and sellers navigate the Denver housing market since 2009.

Categories

- All Blogs (264)

- advice (20)

- broomfield colorado (5)

- buying land (1)

- client experience (8)

- colorado (12)

- Colorado Real Estate Resource Center (168)

- commerce city colorado (2)

- denver metro area (18)

- ELEVATE newsletter (35)

- FAQs (1)

- firestone colorado (1)

- first-time homebuyers (10)

- foothills properties (1)

- for buyers (10)

- for sellers (17)

- government (1)

- home improvements (1)

- home valuation (1)

- homebuyers (24)

- homebuyers in 2025 (15)

- homebuyers in 2026 (14)

- homebuying in 2024 (11)

- inflation (4)

- interior design & decor (1)

- investing/investors (3)

- land surveys (2)

- listings that didn't sell the first time (2)

- local news (34)

- market updates (13)

- matt thomas (3)

- monthly housing updates (28)

- mortgage interest rates (34)

- mortgage lending (23)

- mountain properties (1)

- moving (2)

- national news (32)

- negotiations (2)

- open houses (1)

- opinion (3)

- press release (3)

- property management (2)

- property taxes (2)

- radon (1)

- ReaL Broker (2)

- relocating (4)

- remote homebuying (1)

- rentals (1)

- renting (1)

- selling your home in 2025 (2)

- senior homeowners (2)

- showings (3)

- the altitude group (4)

- thornton colorado (6)

- videos (14)

- vocabulary (4)

Recent Posts

GET MORE INFORMATION

Consultant | Broker Associate | FAFA100030130