Will Fed Rate Cuts Create Opportunity?

Earlier this week we watched (and celebrated) as interest rates finaly fell to their lowest point since they started rising rapidly back in the summer of 2022.

However, if you followed what happened with rates since and are wondering how much lower your mortgage rate quote is after the Federal Reserve met on Wednesday, this is required reading.

Mortgage Minute

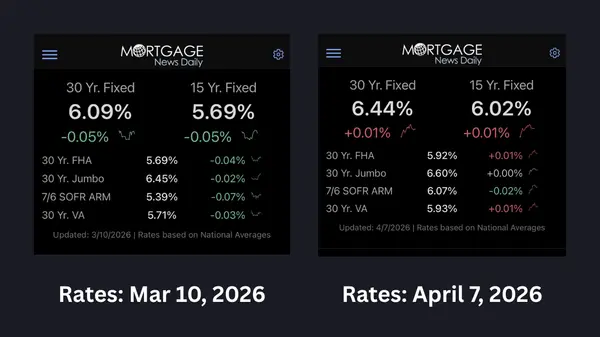

Rates earlier this week (Tuesday) had fallen to three-year lows. Literally the last time rates had been so low is when they started climbing back in 2022. As of Tuesday, interest rates for a mortgage were as low as 6.13%.

Now here we are, just a few days later, and rates are at 6.35%--not bad compared to the last year, but if you've heard the news about the Fed cutting rates, well, that's different than mortgage rates. The juxtaposition of yesterday's Fed rate cut and the sudden mortgage rate spike is incredibly confusing to most of people, so let's clear it up.

Logan Motoshami, of Housingwire summarized the actions of this week this way:

“SHORT VERSION:

• The Fed Funds Rate (FFR) doesn't dictate mortgage rates

• The FFR only changes on Fed announcement days, 8 times a year. It changes in response to various economic reports and events.

• Mortgage rates change daily and the bonds that drive mortgage rates change in real-time throughout the day. That means mortgage rates can drop fo the same reasons that drove yesterday’s rate cut.

• Because those reasons were already in play well before yesterday, mortgage rates had already responded to them well before yesterday.

• Bottom line: the Fed Funds Rate and mortgage rates dropped for the same reasons, but mortgage rates got to do it sooner because they move more nimbly.

LONG VERSION:

• We've written and re-written the long version too many times to count. Here is one of the most evergreen examples:

SPECIAL NOTE REGARDING OTHER NEWS STORIES SAYING RATES ARE LOWER:

There are an unfortunate number of news articles out there today that claim mortgage rates are LOWER. This is due to Freddie Mac's weekly rate survey dropping to 6.26 from 6.35 last week. Freddie's rate is an average of the 5 days ending yesterday, so 80% of the input is comprised of the low rates in a long time. News organization quote the survey and give the impression that this week's rates are lower than last week's.

But what the survey really means is that the average rate from Thursday the 11th through yesterday was lower than the average rate between Thursday the 4th and Wednesday the 10th. You can't go back to the first 3 days of this week and lock those rates, so unequivocally, undoubtedly, and incontrovertibly, the rates you can lock today are absolutely higher than last week's and the average lender is at 2-week highs. There is no question, debate, or nuance to this fact. Anyone who tells you something else is wrong or misinformed. Period."

BOTTOM LINE

When you call your loan officer after the Fed’s cut, don’t expect Tuesday’s rates—but don’t despair either. The best rates in 11 months, and some of the most favorable in three years, are still here. It’s still the Autumn of Opportunity.

Watch last week's Mortgage Minute on YouTube for additional information leading up to the Fed's meeting this past week.

Categories

- All Blogs (264)

- advice (20)

- broomfield colorado (5)

- buying land (1)

- client experience (8)

- colorado (12)

- Colorado Real Estate Resource Center (168)

- commerce city colorado (2)

- denver metro area (18)

- ELEVATE newsletter (35)

- FAQs (1)

- firestone colorado (1)

- first-time homebuyers (10)

- foothills properties (1)

- for buyers (10)

- for sellers (17)

- government (1)

- home improvements (1)

- home valuation (1)

- homebuyers (24)

- homebuyers in 2025 (15)

- homebuyers in 2026 (14)

- homebuying in 2024 (11)

- inflation (4)

- interior design & decor (1)

- investing/investors (3)

- land surveys (2)

- listings that didn't sell the first time (2)

- local news (34)

- market updates (13)

- matt thomas (3)

- monthly housing updates (28)

- mortgage interest rates (34)

- mortgage lending (23)

- mountain properties (1)

- moving (2)

- national news (32)

- negotiations (2)

- open houses (1)

- opinion (3)

- press release (3)

- property management (2)

- property taxes (2)

- radon (1)

- ReaL Broker (2)

- relocating (4)

- remote homebuying (1)

- rentals (1)

- renting (1)

- selling your home in 2025 (2)

- senior homeowners (2)

- showings (3)

- the altitude group (4)

- thornton colorado (6)

- videos (14)

- vocabulary (4)

Recent Posts

Headlines Arrive Last: What Denver Agents Were Already Seeing in the Housing Market

When Rates are Volatile, Just Pivot

Who’s the Best Realtor for Selling a Home in Broadlands in Broomfield?

Who’s the Best Realtor for Selling a Home in Silver Leaf in Broomfield?

Who’s the Best Realtor for Selling a Home in Anthem in Broomfield?

Who’s the Best Realtor for Selling a Home in Wildgrass in Broomfield?

Who’s the Best Realtor for Selling a Home in Lewis Pointe?

Who’s the Best Realtor for Selling a Home in Cherrywood Park?

Who’s the Best Realtor for Selling a Home in The Haven?

Who’s the Best Realtor for Selling a Home in Quail Valley?

GET MORE INFORMATION

Matt Thomas

Consultant | Broker Associate | FAFA100030130